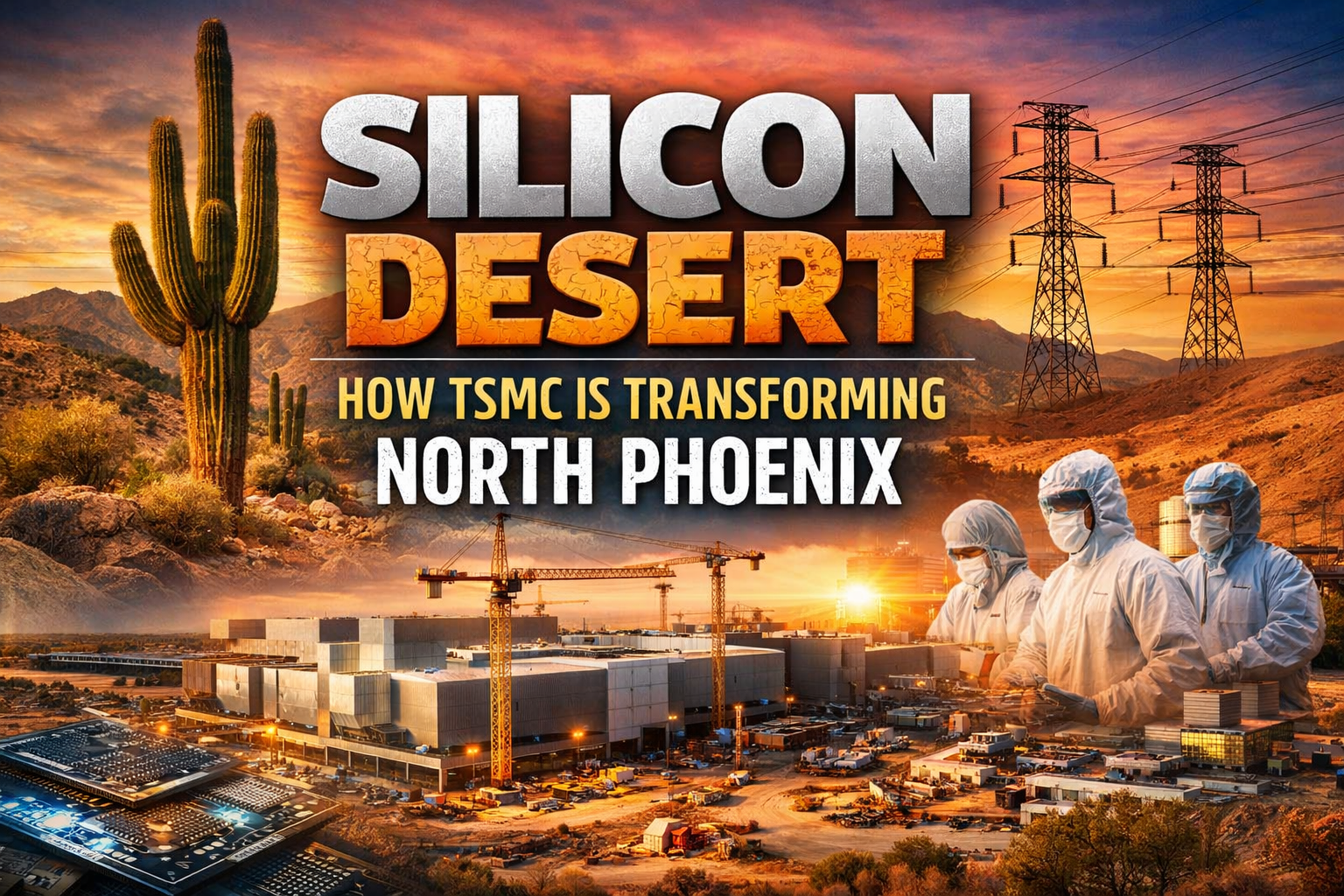

At first glance, the land north of Phoenix still looks like what it has been for decades: pale dirt, creosote bushes, distant mountains wavering in the heat. But drive far enough toward the city’s northern edge—past the last big-box stores and the master-planned communities that taper into open desert—and you hit something that feels out of place. Towering steel structures. Cranes frozen mid-air. A project so large it has its own gravity. This is where the future is being poured, slab by slab.

The expansion of TSMC’s semiconductor campus in Phoenix’s North Gateway has become one of the most consequential industrial investments in modern Arizona history. It’s also one of the least fully understood by the people who live closest to it. Most residents know the headline numbers—tens of billions in investment, thousands of jobs, national security implications. Fewer have grappled with what this actually means on the ground: for housing, infrastructure, and daily life across the North Valley.

A Desert Bet With Global Stakes

This isn’t just a factory story. It’s a city story—still being written.

When TSMC announced its first Arizona fabrication plant in 2020, the move landed like a geopolitical thunderclap. Semiconductors—the invisible components powering everything from vehicles to medical devices—had become the world’s most fragile supply chain. The U.S. wanted domestic production. Taiwan wanted diversification. Arizona emerged as the unlikely middle ground.

According to The Wall Street Journal and Bloomberg, federal incentives from the CHIPS and Science Act later accelerated the project, pushing planned investment beyond $65 billion.

External references:

National coverage frames the move around geopolitics. Locally, the impact is more tangible. Construction traffic. Shift changes. Desert parcels once written off as “someday land” now discussed in terms of logistics hubs, supplier campuses, and housing tracts.

The North Valley is no longer speculative. It’s operational.

Why North Phoenix, and Why Now?

The North Gateway area didn’t land this project by accident. It offered what few metro regions still can: large contiguous land, expandable power infrastructure, and direct access to I-17 without immediate residential displacement.

That buffer is shrinking.

Economic development officials often describe TSMC as a “magnet.” That’s true—but incomplete. Magnets don’t just attract; they reorganize everything nearby. Suppliers cluster. Workforce housing follows. Service businesses fill in the gaps. Urban economists call this agglomeration. Residents call it congestion.

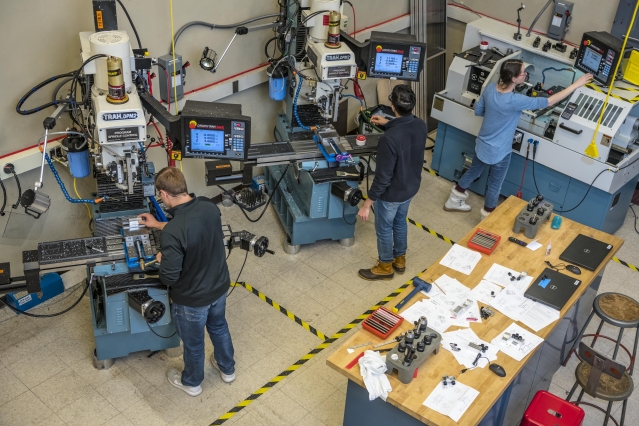

Jobs, Yes—but Not the Ones You Think

The assumption that this is a single-employer boom misses the point. TSMC’s Arizona operations will employ thousands directly, many in high-paying technical roles. But semiconductor manufacturing relies on a dense ecosystem.

A 2023 Semiconductor Industry Association report estimates that every chip-manufacturing job supports four to five additional jobs elsewhere in the economy.

Reference: https://www.semiconductors.org

Many of these roles are skilled trades and technical operations—not just engineering—which has pushed Arizona’s community colleges and universities to expand semiconductor training pipelines.

Industrial policy, here, isn’t theoretical. It’s vocational.

Housing Pressure: The Invisible Side Effect

As construction accelerated, housing demand followed—engineers, contractors, vendors, and service workers all seeking proximity. Builders responded, but entitlement timelines and infrastructure constraints slowed supply.

The result: upward pressure on prices and rents.

Wired has documented similar patterns near new chip fabs in Texas and Ohio, but the North Valley’s transformation is happening faster.

Reference: https://www.wired.com

For longtime residents, the shift feels compressed—decades of growth packed into a few years.

Infrastructure Is Destiny

Factories don’t run on optimism. They require water, power, and redundancy.

Water use has drawn scrutiny, but reporting from Reuters and The Arizona Republic shows TSMC’s Arizona facilities are designed to recycle a majority of the water they consume, relying heavily on reclaimed sources.

References:

Power upgrades tell a parallel story. Substations and transmission improvements built for the fab unlock capacity for everything around it.

In most cities, infrastructure follows growth. Here, growth arrived all at once.

A Desert, Rewired

The North Valley has always been a place of becoming—a region shaped by long horizons and calculated risk. The expansion of TSMC doesn’t change that. It accelerates it.

What’s rising north of Phoenix isn’t just steel and clean rooms. It’s a new role in the global economy, anchored in a place once considered peripheral.

The desert hasn’t disappeared.

It’s been rewired.

And for those who live here, the question isn’t whether change is coming—it’s how intentionally it’s met, and who gets to help shape what comes next.

![Your Journey to Homeownership [INFOGRAPHIC] | MyKCM](https://files.mykcm.com/2021/11/18120549/20211119-MEM-1046x2358.png)